This is the blog post to show how an unknown structural break can be found for any variable. Following illustration is only available in eviews 8 and onward, you can get demo version of eviews from eviews website.

Suppose you have a variable in eviews

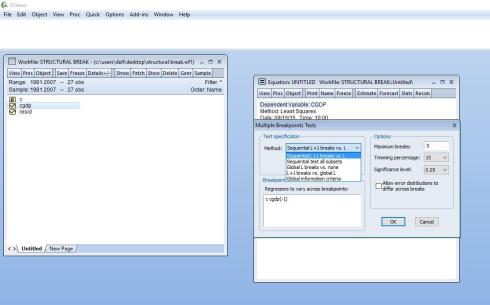

To find the structural break you have to estimate AR(1) model in this the independent variable in the lag of dependent variable

Now go in the stability test you have multiple break-point test

There are 5 methods but go with the first one

It will tests up to 5 breaks in the data and show you the significant ones

In sequential it has provided the three break dates in the order of their significance, as we usually use one break in the model so we take 2003 as a break.

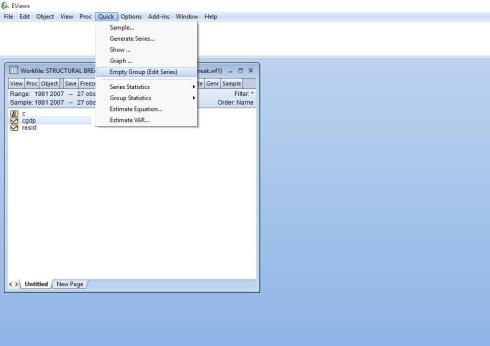

Now we open empty group edit series

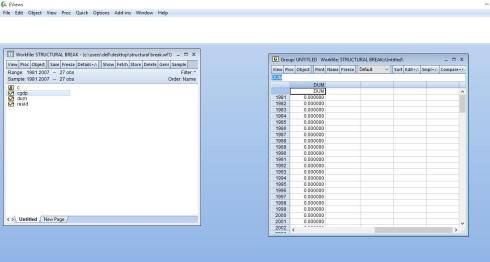

Here we make a new vairable named as dum and write zeros “0” uptil 2002 and write ones “1” from 2003 and onward

This will make a structural break variable. Which can be used in any regression as an independent variable.

Source:

- Perron, Pierre (2006). “Dealing with Structural Breaks,” in Palgrave Handbook of Econometrics, Vol. 1:

Econometric Theory, T. C. Mills and K. Patterson (eds.). New York: Palgrave Macmillan. - Eviews Manual

Thank you for your knowledge. It was so helpful for my research. I am doing my thesis now and it’s about nonlinear ARDL Cointegration. But when I processed my data, the CUSUM test showed unstable model. And i interest to add some structural break time to make CUSUM to be stable. So, if i take your example, when you get 2003 as structural break period. What should you to your new variable (dum)? You wrote “1” just in 2003 or you wrote “1” in 2003-2007? I hope you answer my problem. Thank you.

I wrote 1 from 2003 and onward till 2007

what’s your reason when you wrote the dum from 2003-2007? whereas the program chosen 2003 as the structural break? thanks

as this test is showing permanent break (change) it means it will carry on till the end of the data

And what is the different if i choose sequential L+1 and global information criteria? I hope you answer my problem. Thank you.

I have no idea, kindly refer to the base paper mentioned in the output.

In case, if the CUSUM and CUSUM of square are statistically significant, showing that the estimated coefficients are stable then is it necessary to run the chow test??

no need. Cusum and CUSUM sq is advanced version of chow test

Thanks a lot for all your effort to support scientific research, if i have 6 variables in my model ( 1 dependent and 5 independent) my data 31 years, i want to applied breakpoint test in order creat dummy varible.

what i should do in this case:

1- I should make one dummy for all variables together, Please explain how?

2- or I should make dummy for evry variable As explained in the example above ( it means 6 dummy variables)?

This problem really confused me. I am waiting for your help .

if you want to use the break in regression then make the break for the dependent variable only

thank you for the time and effort you put into this.

could you please explain more ?!

I have the same problem here

Watch youtube channel of IHS which has made eviews, there are several relevant help tutorials